Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

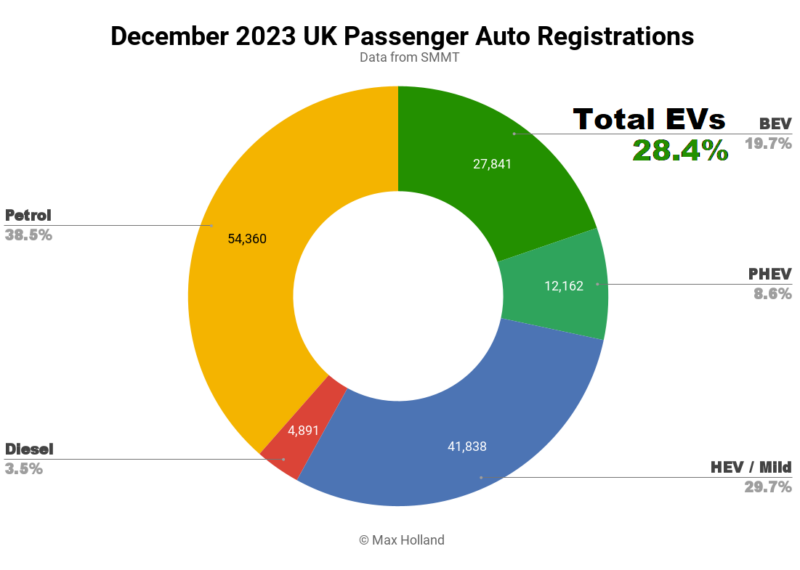

December saw plugin EVs take 28.4% share of the UK auto market, down YoY from 39.4%, as deliveries were held back to meet new 2024 mandates. Full year 2023 BEV volume was up by 18% from 2022. December’s overall auto volume was 141,092 units, up 10% YoY. Tesla was December’s leading BEV brand, and the Tesla Model Y was 2023’s bestselling BEV.

December saw combined EVs take 28.4% share, with full electrics (BEVs) taking 19.7%, and plugin hybrids (PHEVs) taking 8.6%. These compare with shares of 39.4% combined, 32.9% BEV, and 6.5% PHEV, a year ago.

December’s year on year comparison looks weak, partly because the end of 2023 experienced a hold-back ahead of a policy change coming into effect in 2024. The new 2024 ZEV mandate requires auto manufacturers to meet a minimum share of 22% ZEV sales for the full year (and getting higher in future years). For a reminder of the new rules, check my report from last month.

Holding back some proportion of Q4 2023 deliveries until Q1 2024 helps manufacturers meet the tight new 2024 targets and avoid very substantial fines. How much are the fines? Up to £15,000 (€17,420) for every non-BEV that they sell. Since 2024 BEV registrations have such substantial monetary value (in fines avoided) for manufacturers, why not hold back a few from late 2023 (where they have no such value), and put them to work towards the new 2024 targets instead?

If this is indeed what is happening (and other analysts have independently made the same suggestion, here and here), Q1 2024 should bounce back to higher than average BEV share, as the delayed deliveries are finally fulfilled.

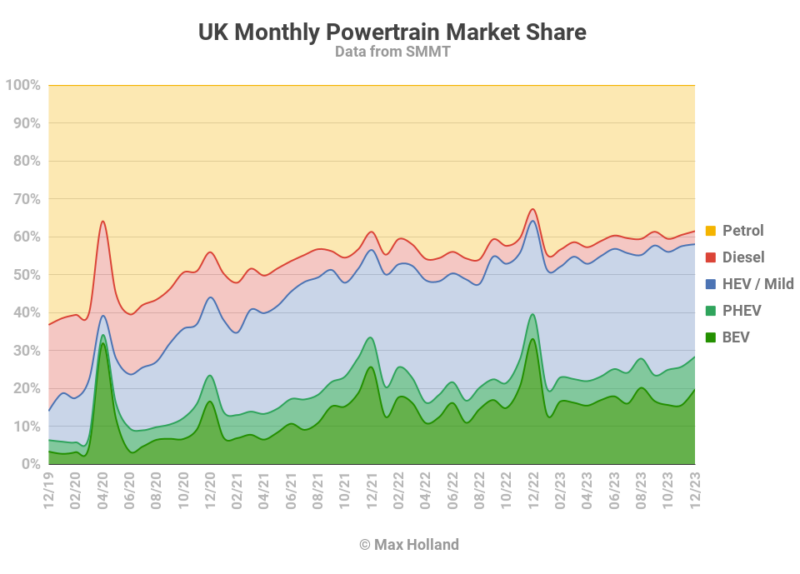

Partly because of the Q4 hold-back, full year 2023 BEV headline performance looks unimpressive, with share of just 16.5% compared to 16.6% for full year 2022.

Without the new rules distorting the Q4 figures, however, the underlying performance was a bit better. BEV sales volume by the end of Q3 was at 238,541 units, up a healthy 35.8% from the same period in 2022. This came against the background of overall auto volume growth of 20.2%, thus somewhat suppressing BEVs’ improvement in share — only up to 16.4% by Q3 end, from 14.5% at the same point in 2022.

Taking a step back, UK overall auto volumes are now just 18% below the 2011-2019 average, so any future recovery in overall volume has an upper limit. This means that future (and continuing) increases in BEV volume will translate more proportionally into improvement in market share.

Meanwhile, ICE vehicles continue their downward trend in share. Petrol-only vehicles have spent the past 2 months at under 40% market share, which is a new record. Diesel-only vehicles have spent the past 4 months at under 4% market share, also a new record. We can expect to see their combined share dip below 40% by H2 2024, if not earlier.

Top BEV Brands

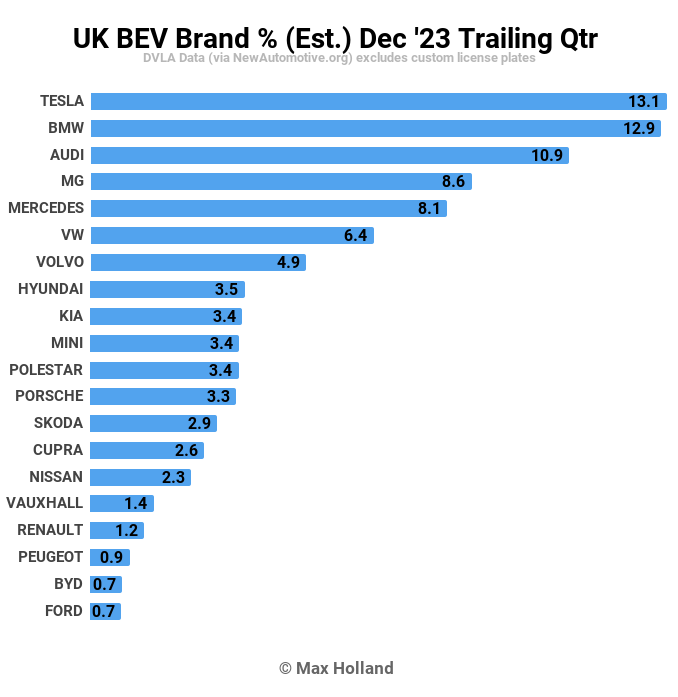

Tesla was back to the top spot for BEV brands in December, taking 19.8% of the BEV market. This is a recovery from November and October, where Audi, and BMW (respectively), took the top spot.

Given that the UK is a right hand drive market, irregular batching of deliveries is somewhat inevitable by brands, so let’s take a look at the trailing 3 month figures to smooth out the monthly variabilities:

Here, the situation is much more even, with BMW almost matching Tesla for market share, and Audi not very far behind. Since the prior period (July to September), BMW increased volumes by 1.27x, and Audi by 1.36x. For Tesla, on the other hand, volume fell to just 0.73x of the previous amount.

Another good improvement was seen by Volvo, with 2x volume increase, enough to take 7th spot, from 15th previously. BYD managed to squeeze into the top 20 brands for the first time, at 19th, having launched volume deliveries back in September.

Now let’s look at the full year top 5 brands:

Tesla’s good momentum in the first half of the year helped it pull out a large lead over the others. MG had a strong performance in Q3, which helped it stay ahead of BMW and Audi over the full year. For more full year data, see my graphs elsewhere.

At the end of year, the UK industry body, the SMMT, provides a list of the top 10 best selling BEV models for the full year. Unsurprisingly, Tesla took the top spot with the Model Y, with 35,899 units, enough to also put it in 5th place in the overall list (left side column):

The Model Y saw just a modest increase (of 348 units) in 2023 full year volume compared to 2022. Since the overall market — and most other popular models — grew volume by some 18%, this pushed the Model Y down to 5th, from 2022’s 3rd ranking. Still a good result considering that no other BEV yet gets close to the overall top 10.

Outlook

The UK’s auto market annual growth of 18% in 2023 was a brighter spot than the overall economy, which hovered at 0.3% annual growth in GDP in both Q2 and in Q3 (latest data) and may trend lower in Q4. The inflation rate cooled in November to 3.9%, but interest rates stayed flat at 5.25%. Manufacturing PMI fell to 46.2 points in December, from a recent high of 47.2 points in November.

The SMMT did not mention the BEV hold-back strategy of its member companies in Q4, but instead asked for more government support for consumer BEV purchases. The SMMT CEO said “Government has challenged the UK automotive sector with the world’s boldest transition timeline and is investing to ensure we are a major maker of electric vehicles. It must now help all drivers buy into this future, with consumer incentives that will make the UK the leading European market for ZEVs.” (SMMT)

They are asking that VAT on BEVs be halved to 10% going forwards, to help meet the growth goals. This would help (the more laggard) manufacturers meet their 2024 mandates, by effectively making the on-the-road price for BEVs 9.1% lower than it otherwise might be, helping them sell more units. It would also help private consumers a bit, in the short term, by reducing the entry price to get into a new BEV. It would hurt recent new owners of BEVs by reducing their residual value by 9.1% overnight. In the long run, it might marginally delay the efforts of manufacturers to find BEV cost efficiencies on their own — by aiming for economies of scale via high volumes, and more R&D investment. This would then delay the timeline for BEVs to outcompete ICEs on (unadulterated) market pricing.

Anyway, we will see BEV share of at least 22% in 2024 (though the actual figures are a bit more messy) due to the new ZEV mandate. The coming few months will be interesting to watch. What do you think? Please jump in to the comments below to join the discussion.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Our Latest EVObsession Video

I don’t like paywalls. You don’t like paywalls. Who likes paywalls? Here at CleanTechnica, we implemented a limited paywall for a while, but it always felt wrong — and it was always tough to decide what we should put behind there. In theory, your most exclusive and best content goes behind a paywall. But then fewer people read it!! So, we’ve decided to completely nix paywalls here at CleanTechnica. But…

Thank you!

CleanTechnica uses affiliate links. See our policy here.