Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

One of the interesting notes in the recently published US Solar Market Insight report is that the average global solar module price in the 3rd quarter of 2023 was down 30–40% from the average global solar module price in the 1st quarter of 2023. This is primarily due to supply–demand imbalances in China. The US market gets almost no solar panels from China due to tariffs and the Uyghur Forced Labor Prevention Act (UFLPA), with those Chinese solar panels accounting for just 0.1% of US solar module imports. Nonetheless, those global trends have had notable ripple effects on US solar module prices, which were down 15% in Q3 2023 compared to Q1 2023.

“However, it’s important to acknowledge the differences in solar module supply dynamics between the US and the rest of the world. Other global regions are currently in a state of module oversupply. As China continues its massive expansion of manufacturing capacity across the entire solar value chain, there has been significant downward pressure on global module pricing. The impacts of this oversupply situation have escalated recently, with reports of spot module prices outside of the US as low as 14-15 cents/watt,” the report states.

“By contrast, the US market is somewhat insulated from these pricing dynamics. Less than 0.1% of US module imports this year have come from China due to a combination of tariffs (anti-dumping and countervailing duties [AD/CVD], Section 201, and Section 301). Almost 80% of modules for the utility-scale market come from Southeast Asia. And while Southeast Asia is generally a low-cost region for module production, manufacturers are still exposed to the restrictions on polysilicon sourcing from China due to the Uyghur Forced Labor Prevention Act (UFLPA).

“Consequently, module supply to the US utility-scale sector is still tighter than other global regions. Demand for modules from top tier 1 manufacturers is high. This has kept US module pricing significantly above price points in other countries, even without anticircumvention tariffs (for more on solar component pricing, see Wood Mackenzie’s PV Pulse). On balance, availability of modules for the US utility-scale market is still constrained but has improved substantially this year. Of course, module availability will continue to improve as more domestic manufacturing comes online.”

What’s surprising and a bit crazy is that the utility-scale solar power market is having much more trouble now getting other parts. Solar module supplies have started flowing pretty well, but the industry has to wait a long time for other types of electrical equipment. The result, naturally, is also rising prices. “Transformer availability has become a widespread problem, with wait times extending past 2 years in some cases. High-voltage circuit breaker lead times have nearly doubled in the last year to an average of 100 weeks (see Wood Mackenzie’s report H2 2023 US solar PV system pricing). This has already increased balance of system (BOS) pricing for utility-scale solar. With no signs of this trend reversing, we expect electrical equipment availability to be one of several factors slowing utility-scale solar growth in the next several years.”

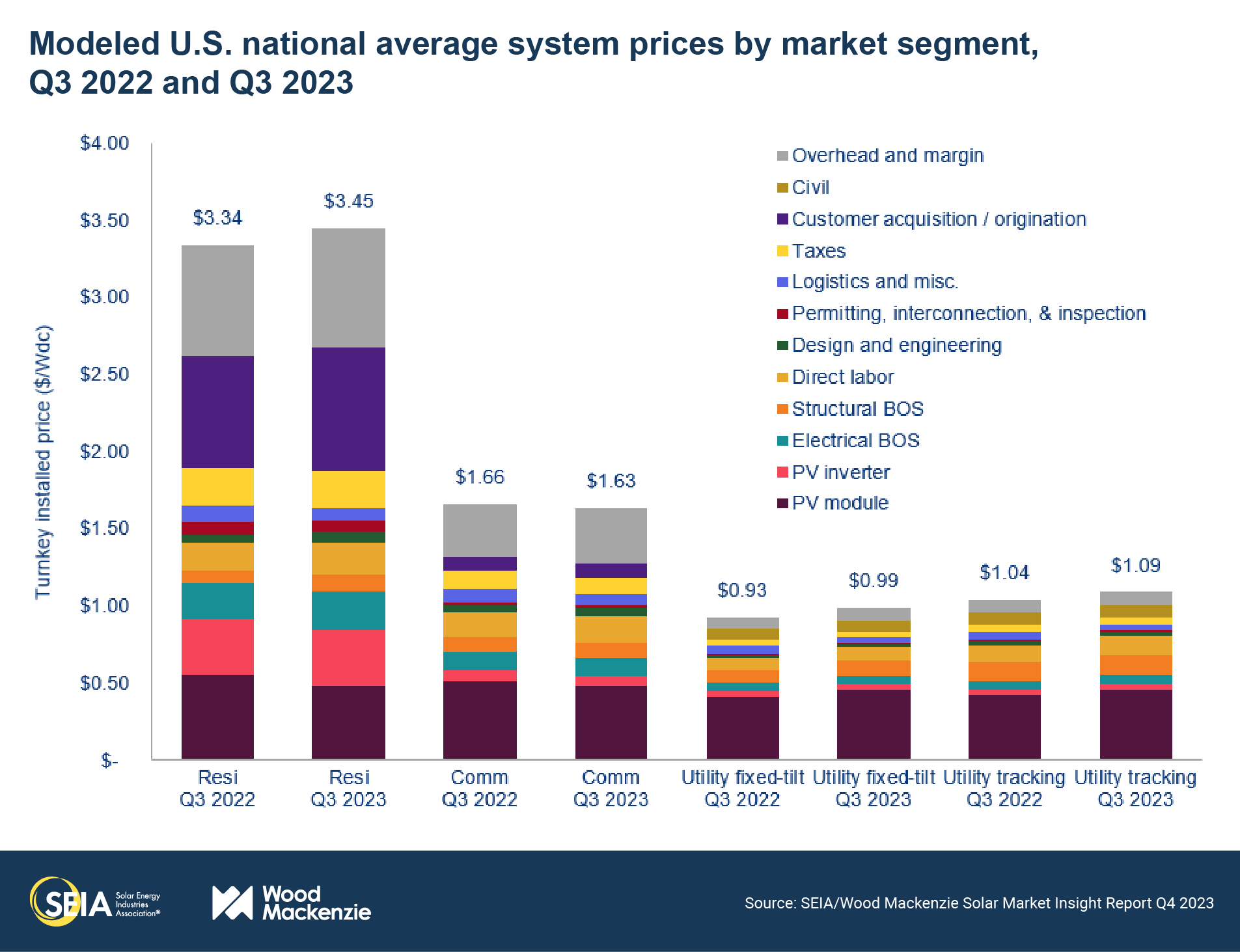

If we break it down by sector (chart above), we see that residential solar power system pricing was up 3%, commercial solar power system pricing was down 2%, and utility-scale solar power system pricing was up 5% (single-axis trackers) to 6% (fixed-tilt systems).

Here are more details on how the pricing for these different segments was split out by component: “Module prices declined 12% for the residential and 6% for the commercial segment year-over-year. The utility segment continues to see elevated module pricing due to the one-year lag in module procurement reflected in our pricing data. For distributed solar, the decline in module costs has been offset by an increase in the balance of equipment as well as soft costs. Across the four different market segments, labor and engineering costs have increased anywhere from 5-25%. Equipment component costs have also been increasing over the last few quarters due to the rise in inflation. National PV system prices are up across all segments except for the commercial segment, which witnessed a drop of 2% year over year.”

We’ll see what happens in Q4 and in 2024, but it’s clear there are a variety of factors influencing pricing, including differences between the market segments. It’s hard to know how much will change in the coming months, as the economic and political situations feels a bit up in the air and susceptible to strong shifts in the trends. We shall see.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Our Latest EVObsession Video

I don’t like paywalls. You don’t like paywalls. Who likes paywalls? Here at CleanTechnica, we implemented a limited paywall for a while, but it always felt wrong — and it was always tough to decide what we should put behind there. In theory, your most exclusive and best content goes behind a paywall. But then fewer people read it!! So, we’ve decided to completely nix paywalls here at CleanTechnica. But…

Thank you!

CleanTechnica uses affiliate links. See our policy here.